Managing international finances requires a balance of timing, strategy, and a deep understanding of tax regulations. For the Indian diaspora in the United States, 2026 has brought several pivotal updates to how wealth is transferred across borders. One of the most significant figures to keep in mind this year is $19,000 the IRS annual gift tax exclusion limit. Understanding this threshold is the first step in ensuring that your generous support for family or investments remains protected from unnecessary tax liabilities.

When you prepare to transfer money from usa to india, being aware of the annual exclusion helps you plan your contributions without the immediate need for complex tax filings. This $19,000 limit applies per recipient, meaning you can provide this amount to multiple family members such as your parents, siblings, or spouse individually, all within the same calendar year, while keeping your financial footprint efficient and compliant.

Decoding the $19,000 Annual Exclusion for 2026

The Internal Revenue Service (IRS) adjusts the annual gift tax exclusion based on inflation, and for 2026, the limit has been set at $19,000. This is the amount you can give to any single individual without having to file a gift tax return (Form 709).

For married couples, this benefit effectively doubles. Through “gift splitting,” a husband and wife can collectively send up to $38,000 to a single recipient in India tax-free. This is particularly beneficial for those funding major life events, such as a sibling’s wedding, a down payment on a family home, or comprehensive medical care for elderly parents.

Key Highlights of the 2026 Rule:

- Per-Recipient Limit: You can give $19,000 to any number of people. If you have three siblings in India, you could send $19,000 to each ($57,000 total) without triggering a gift tax return.

- No Tax for Recipients: Under the Foreign Exchange Management Act (FEMA) in India, money received from relatives for family maintenance or as a gift is generally tax-free in the hands of the recipient.

- Direct Payments: Payments made directly to educational institutions or medical providers for someone else’s benefit do not count toward the $19,000 limit. This allows for even greater support beyond the annual exclusion.

The Role of the “One Big Beautiful Bill Act”

The 2026 tax landscape is also influenced by the “One Big Beautiful Bill Act” (OBBB Act), which has established a robust lifetime estate and gift tax exemption. For 2026, this lifetime limit has risen to $15 million per individual.

What does this mean for your transfers? Even if you decide to send more than $19,000 to a single person, you still likely won’t owe any out-of-pocket gift tax. Instead, the amount over $19,000 simply reduces your $15 million lifetime “bucket.” For example, if you send $25,000 to your mother, the first $19,000 is excluded, and the remaining $6,000 is deducted from your $15 million lifetime exemption. While you would need to file Form 709 to report the $6,000, no actual tax payment is required until that $15 million total is exhausted.

Choosing the Best Path for Your Funds

To truly maximize your wealth preservation, the method of transfer is just as important as the amount. In 2026, digital financial platforms have become the gold standard for high-value remittances. Using these channels ensures that you avoid the 1% excise tax that the OBBB Act applies to transfers funded by physical cash or money orders.

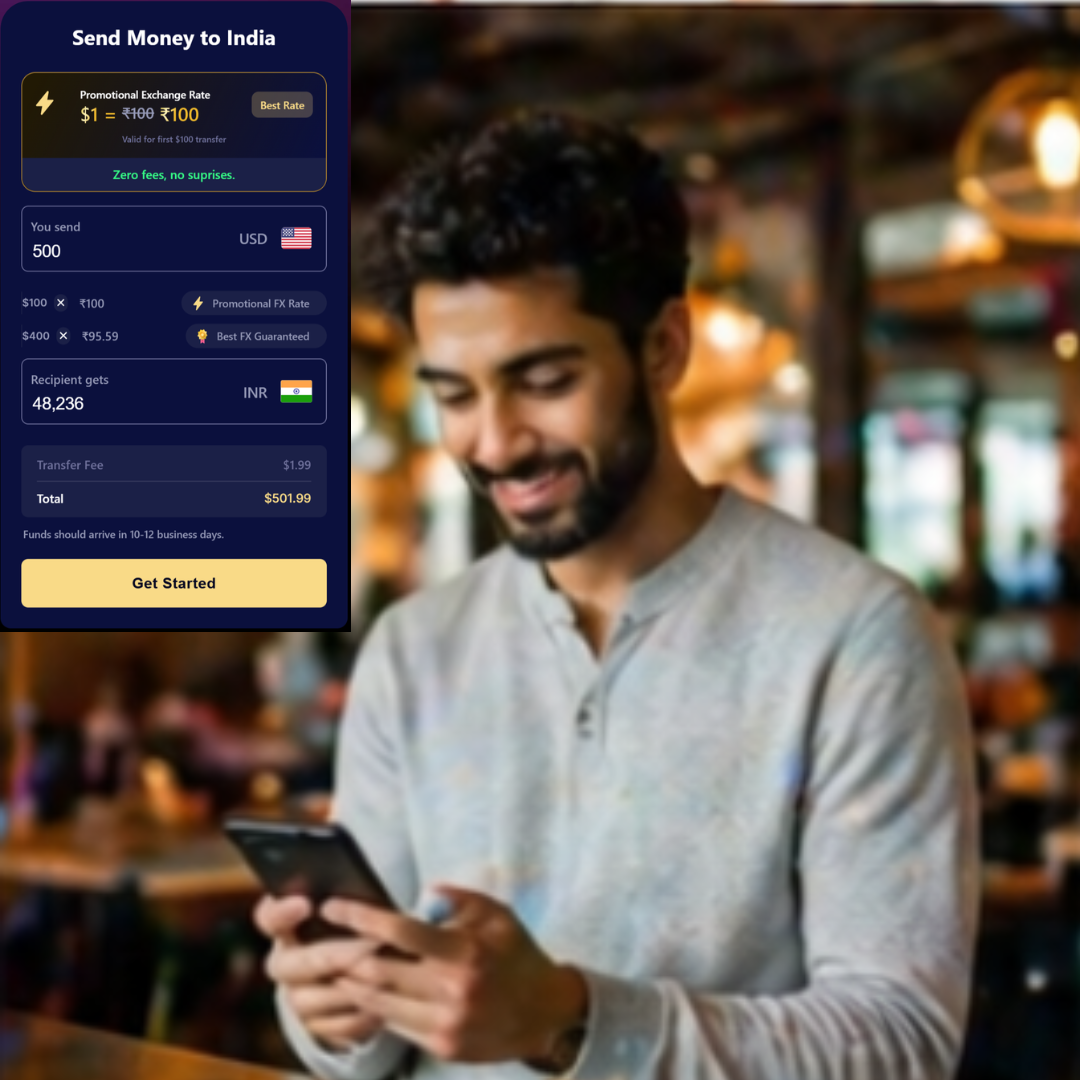

If you are looking for the send money to india best rate, sticking to bank-linked digital apps is the most effective strategy. These platforms pull funds directly from your U.S. bank account, qualifying your transaction as a digital transfer and keeping it exempt from the 1% surcharge. Furthermore, digital platforms often provide better exchange rates and lower service fees than traditional brick-and-mortar agents, ensuring more of your $19,000 reaches your loved ones.

Tips for High-Value Remittances:

- Use Purpose Codes Correctly: When you send money to india, ensure you select the appropriate RBI purpose code (e.g., family maintenance or gift). This helps the recipient bank in India process the funds correctly under FEMA guidelines.

- Maintain Records: Save your digital receipts and Foreign Inward Remittance Certificates (FIRC). These are essential proof that the funds were legally transferred and are often required for property purchases or tax audits in India.

- Compare Totals: Always check the “final amount delivered” rather than just the headline exchange rate. A platform might offer a slightly better rate but have higher hidden fees.

Strategic Timing for Your Transfers

Wealth protection is also about timing. Since the $19,000 exclusion is based on the calendar year (January 1 to December 31), many families choose to spread their support across two years. If you intend to send $35,000 for a specific project, sending $17,500 in late December and the remaining $17,500 in early January allows you to stay within the annual exclusion for both years, completely avoiding the need to file Form 709.

By staying proactive and utilizing modern financial tools, you can ensure that your global financial goals are met with precision and security. The combination of a high annual exclusion and efficient digital pathways makes it an excellent time to plan for your family’s future in India.

Conclusion

Understanding the intersection of U.S. tax laws and Indian financial regulations is the key to successful cross-border wealth management. The $19,000 annual exclusion for 2026 provides a generous window for supporting your loved ones while maintaining a clean tax record. By choosing digital-first transfer methods, you not only avoid new surcharges but also gain access to the competitive exchange rates necessary for high-value transactions. As you plan your next move, remember that a well-informed strategy is your best tool for ensuring that your hard-earned savings provide the maximum possible benefit for your family back home.

Frequently Asked Questions

Can I send $19,000 to my cousin and my brother in the same year?

Yes. The $19,000 IRS annual exclusion is per recipient. You can give up to $19,000 to as many individuals as you wish without triggering a gift tax return filing.

What is the best rate to send money to india for large amounts?

For amounts near the $19,000 limit, digital platforms that offer mid-market exchange rates and transparent, low fees usually provide the best value. Always verify that the platform is a regulated money transmitter to ensure the security of your high-value transfer.

Does the recipient in India have to pay income tax on a $19,000 gift?

If the recipient is a “relative” as defined by the Indian Income Tax Act (including parents, siblings, and spouse), the gift is completely tax-exempt for them. If the recipient is a non-relative (like a friend), amounts over ₹50,000 (approx. $600) may be taxable as income for the recipient.

What happens if I send $20,000 instead of $19,000?

You will need to file IRS Form 709 with your tax return to report the $1,000 excess. However, you likely won’t pay any tax; the $1,000 will just be subtracted from your $15 million lifetime exemption limit.

Are there limits on how much I can send for medical bills?

The IRS allows unlimited tax-free gifts for medical expenses, provided the payment is made directly to the medical institution or provider. If you send the money to a family member’s personal account first, it counts toward your $19,000 annual exclusion.

alok dubey