Global IV Bags Market Size and Forecast

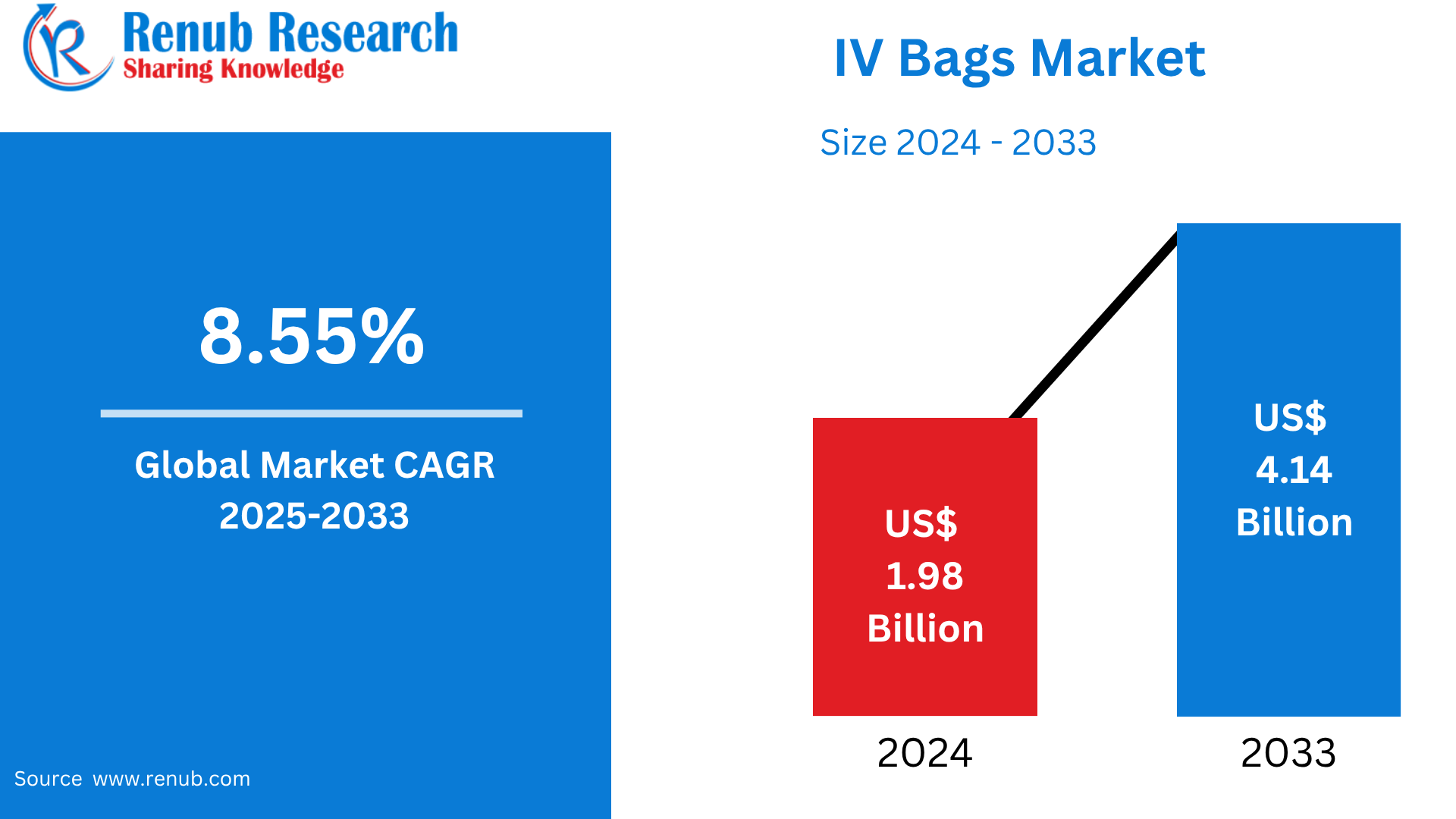

According to Renub Research Global IV Bags Market is set to witness substantial expansion, expected to reach US$ 4.14 billion by 2033, rising from US$ 1.98 billion in 2024, reflecting a steady CAGR of 8.55% between 2025 and 2033. This impressive growth is primarily fueled by increasing hospitalization rates, a surge in surgical operations, rising chronic disease prevalence, expanding elderly population, and the escalating need for sterile, safe, and reliable intravenous fluid delivery systems worldwide. Both advanced healthcare systems and emerging economies are significantly boosting demand as healthcare accessibility improves and patient care standards evolve.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=iV-bags-market-p.php

Global IV Bags Market Outlook

Intravenous (IV) bags are sterile medical containers used to administer essential fluids, medications, nutrients, and electrolytes directly into a patient’s bloodstream. Manufactured using PVC, non-PVC materials such as polyethylene and polypropylene, and glass, these bags are vital in hospitals, clinics, ambulatory care centers, emergency rooms, and long-term healthcare facilities.

IV bags are indispensable in hydration therapy, electrolyte stabilization, blood transfusion, drug infusion, parenteral nutrition, and critical care interventions. They support surgical procedures, intensive care treatments, emergency medicine, and chronic illness management. As global healthcare infrastructure strengthens, alongside technological advancements and patient safety initiatives, the adoption of IV bags is accelerating. The market is increasingly being shaped by innovations in material safety, sustainability initiatives, product sterility enhancements, and expanding usage in home healthcare environments.

Key Market Growth Drivers

Increasing Hospitalizations and Rising Surgical Procedures

The growing global burden of chronic diseases such as cardiovascular disorders, cancer, diabetes, renal conditions, and respiratory illnesses has significantly increased hospital admissions. Higher surgical volumes, especially within trauma care, cardiac surgery, oncology treatments, organ transplants, and emergency procedures, are intensifying demand for IV bags. Additionally, the rise of outpatient surgical facilities and emergency medical units further drives consumption.

Worldwide healthcare expansion, especially in Asia-Pacific, Latin America, and Middle Eastern regions, creates substantial growth opportunities. Hospitals rely heavily on IV therapy as a standard medical practice. With cardiovascular diseases causing nearly 18 million deaths annually, cancer accounting for around 9 million deaths, and millions more impacted by diabetes and respiratory illness, IV therapy remains essential to global patient management.

Shift Toward Non-PVC and Environmentally Safer IV Bags

Concerns surrounding PVC and DEHP-related toxicity are accelerating the global transition toward safer, eco-friendly alternatives. Non-PVC materials such as polyethylene and polypropylene are gaining increasing adoption due to enhanced patient safety, durability, and recyclability.

Healthcare organizations, guided by U.S. FDA standards and EU environmental regulations like REACH, are advancing toward sustainable medical practices. Leading manufacturers are investing heavily in research to develop compliant, cost-efficient, and greener IV bag solutions. For instance, Baxter’s recycling pilot program successfully diverted over 6 tons of PVC waste from landfills, marking a milestone in sustainable healthcare innovation.

Expansion of Home Healthcare and Ambulatory Services

Rising healthcare costs, aging populations, and preference for patient-centric care are boosting home healthcare adoption. IV therapy in home and ambulatory environments requires safe, portable, and reliable IV bag systems, particularly for hydration, chronic disease treatment, pain management, and nutritional support.

Technological advancements in infusion therapy and miniaturized devices enhance home-based treatment efficacy. FDA approvals, such as the introduction of premixed epinephrine IV bags, highlight growing innovation, ensuring convenience, sterility, and reduced need for onsite compounding.

Major Market Challenges

Volatility in Raw Material Prices

IV bag manufacturing relies heavily on petrochemical-derived polymers, making the industry vulnerable to oil price fluctuations and global supply chain instability. Cost volatility impacts production margins, pricing strategies, and affordability across developing healthcare markets. Manufacturers must pursue strategic sourcing, long-term raw material contracts, and innovative production models to ensure cost stability and market continuity.

Stringent Regulatory Frameworks

As critical medical devices, IV bags undergo rigorous regulatory scrutiny from FDA, EMA, ISO, and national health authorities. Compliance requires extensive testing, documentation, quality audits, and global certification — increasing development timelines and production costs. Differences in regulatory standards across countries further complicate large-scale manufacturing for international markets. Non-compliance risks also damage brand credibility and profitability through recalls and penalties.

Material Type Market Insights

Polyethylene IV Bags Market

Polyethylene IV bags are experiencing rising demand as DEHP-free, non-toxic alternatives, ideal for oncology, neonatal, and critical-care environments. Offering excellent barrier protection and high durability, they are gaining strong adoption across North America and Europe, supported by regulatory encouragement and hospital preferences for safer medical consumables.

Polypropylene IV Bags Market

Polypropylene IV bags deliver exceptional chemical resistance, thermal stability, and reduced leachability, making them suitable for parenteral nutrition and long-duration medication storage. Their compatibility with sterilization processes and minimal risk of drug interaction positions them as a preferred solution across Europe and Asia-Pacific, where pharmaceutical innovation and patient safety are top priorities.

Capacity-Based Market Insights

250–500 ml IV Bags Segment

The 250–500 ml segment remains among the most widely used IV bag capacities worldwide. Ideal for medication infusion, electrolyte stabilization, rehydration therapy, and pediatric to adult care needs, this category experiences consistently high demand in hospitals, emergency care, and home healthcare environments. Manufacturers continue improving product sterility, portability, and structural design.

Chamber Type Market Insights

Single-Chamber IV Bags

Holding the largest market share, single-chamber IV bags dominate global usage due to cost efficiency, ease of production, and universal applicability. They are integral in hydration therapy, critical care, drug administration, and routine hospital care. Their increasing adoption in developing economies strengthens market expansion.

Regional Market Highlights

United States

The U.S. leads the global market with advanced healthcare infrastructure, high surgical case volumes, chronic disease prevalence, and strong adoption of non-PVC IV solutions. Growing demand for home infusion therapy and innovation-driven medical product development solidify the nation’s market leadership.

France

France stands out in the European landscape through strong public healthcare support, demand for eco-friendly IV solutions, and national initiatives to boost domestic production post-pandemic. Strict safety standards make it a strategic market for premium IV bag innovation.

India

India is witnessing rapid market growth driven by hospital expansion, medical tourism, increased disease awareness, and national healthcare reforms such as Ayushman Bharat. Domestic manufacturing capabilities are strengthening, while demand for DEHP-free IV bags continues to rise.

Mexico

Mexico benefits from healthcare modernization, rising chronic illness cases, and increasing adoption across public and private healthcare sectors. Strong pharmaceutical manufacturing capabilities and proximity to North American markets make Mexico a strategic regional hub.

Saudi Arabia

Under Vision 2030, Saudi Arabia is investing heavily in healthcare modernization, infrastructure expansion, chronic disease treatment, and domestic manufacturing of medical supplies. Demand for sterile, high-quality IV bags continues to escalate.

Global IV Bags Market Segmentation

Material Type: Polyethylene, Polyvinyl Chloride, Polypropylene, Others

Capacity: 0–250 ml, 250–500 ml, 500–1000 ml

Chamber Type: Single Chamber, Multi-Chamber

Regional Coverage:

North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Competitive Landscape

Leading companies are focusing on sustainable materials, regulatory compliance, technological advancements, and expanded manufacturing to strengthen market positioning. Key players include:

Baxter International Inc.

Kraton Corporation

Technoflex

B. Braun Medical Inc.

Sippex IV Bags

Polycine GmbH

ICU Medical Inc.

Fresenius Kabi

Haemotronic

MedicoPack

These players emphasize innovation, environmental responsibility, R&D investments, partnerships, and capacity expansion strategies.

Conclusion

The Global IV Bags Market is poised for sustained growth, driven by expanding healthcare needs, evolving patient safety standards, technological progress, and widespread hospital reliance on sterile fluid therapy solutions. The transition toward non-PVC, eco-friendly IV bags, rising home care integration, and strengthening healthcare infrastructure worldwide will continue shaping the industry’s future.

renubresearch