Europe STD Diagnostics Market Size and Forecast 2026–2034

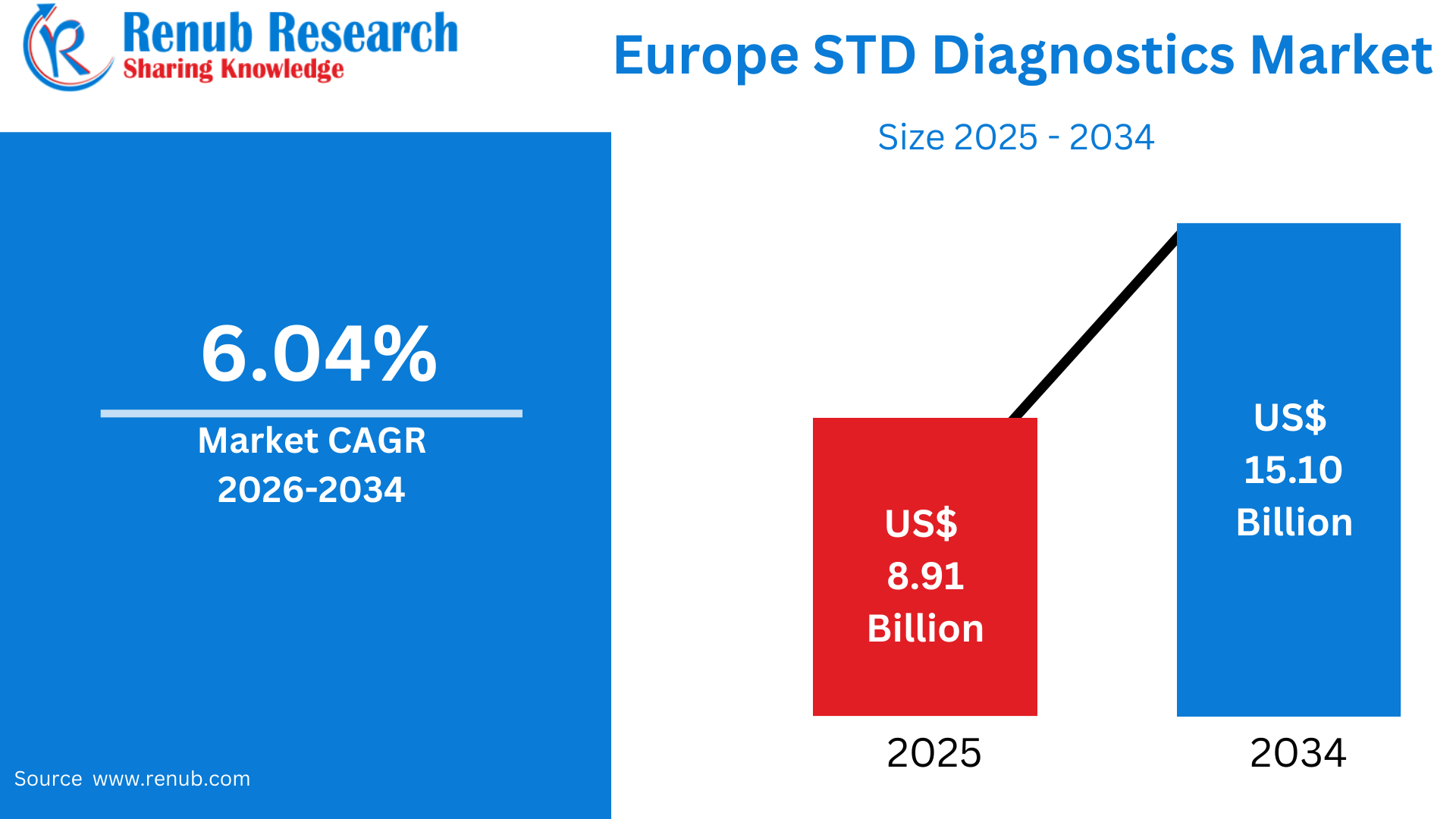

According to Renub Research Europe STD diagnostics market is expected to witness steady and sustained growth during the forecast period, expanding from USD 8.91 billion in 2025 to USD 15.10 billion by 2034, at a compound annual growth rate (CAGR) of 6.04% from 2026 to 2034. This growth is primarily driven by the rising prevalence of sexually transmitted diseases (STDs), increased awareness and screening initiatives, and continuous technological advancements in diagnostic platforms. Europe’s well-established healthcare infrastructure, combined with government-backed preventive healthcare programs and improved access to testing services, continues to strengthen demand for STD diagnostics across the region.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=europe-std-diagnostics-market-p.php

Europe STD Diagnostics Market Overview

STD diagnostics refers to a broad range of laboratory-based and point-of-care tests used to identify sexually transmitted infections such as chlamydia, gonorrhea, syphilis, HIV, HPV, and herpes simplex virus. These diagnostic solutions include serological assays, molecular diagnostics such as polymerase chain reaction (PCR), rapid antigen and antibody tests, multiplex panels, and emerging self-testing solutions. The primary objective of STD diagnostics is early and accurate detection, enabling timely treatment, preventing complications, and reducing disease transmission.

In Europe, increasing STD incidence rates and growing public health focus on disease surveillance have elevated the importance of routine and preventive STD testing. Healthcare systems actively encourage screening among high-risk populations, including sexually active young adults, men who have sex with men, pregnant women, and immunocompromised individuals. Widespread access to confidential and fast testing, combined with reduced social stigma through education and awareness campaigns, has significantly improved acceptance and utilization of STD diagnostic services across European countries.

Europe STD Diagnostics Market Outlook

The European STD diagnostics market benefits from a technologically advanced healthcare ecosystem that supports the adoption of sophisticated diagnostic platforms. Centralized laboratories, hospital networks, and specialized sexual health clinics increasingly rely on molecular and multiplex testing systems due to their superior sensitivity, specificity, and scalability. At the same time, decentralized testing solutions such as rapid point-of-care and home-based self-testing kits are gaining popularity due to convenience, privacy, and faster turnaround times.

Growing integration of digital health technologies, laboratory automation, and connectivity with electronic medical records further enhances diagnostic efficiency. Europe’s focus on preventive healthcare, early detection, and infection control ensures continued investment in STD diagnostic infrastructure, positioning the market for long-term expansion.

Market Changer in the European STD Diagnostics Industry

Rising Burden of Sexually Transmitted Diseases

The increasing prevalence of sexually transmitted infections across Europe is one of the most influential drivers of market growth. Rising cases of chlamydia, gonorrhea, syphilis, and HIV have intensified the demand for early, routine, and repeat testing. Changes in sexual behavior, increased urbanization, improved disease reporting, and heightened awareness among populations have contributed to higher testing volumes.

Public health authorities across Europe actively promote screening programs targeting high-risk groups. Surveillance data from the European Centre for Disease Prevention and Control indicates a significant rise in reported gonorrhea cases, reaching nearly 100,000 annually, a sharp increase compared to previous years. This growing disease burden underscores the urgent need for reliable, scalable, and accessible diagnostic solutions.

Technological Advancements in Diagnostic Solutions

Technological innovation plays a pivotal role in shaping the Europe STD diagnostics market. Advances in molecular diagnostics, automation, and digital platforms have significantly improved diagnostic accuracy, reduced turnaround times, and increased laboratory throughput. PCR-based assays are now widely adopted for infections such as chlamydia and gonorrhea due to their high sensitivity and specificity.

Multiplex testing technology represents a major advancement, enabling simultaneous detection of multiple pathogens from a single sample. This approach improves efficiency, reduces costs, and supports comprehensive screening strategies. Improvements in assay performance have strengthened clinician confidence and expanded the use of advanced diagnostics in both centralized and decentralized healthcare settings.

Increased Availability of Screening and Preventive Healthcare Programs

Government-supported screening and preventive healthcare programs are critical growth catalysts for STD diagnostics in Europe. National and regional initiatives emphasize early detection, routine testing, and repeat screening to control disease spread and prevent long-term complications. These programs often target vulnerable populations and prioritize infections linked to severe outcomes, including infertility, cancer, and congenital conditions.

Large-scale initiatives funded through EU health programs aim to improve access to vaccination, testing, and treatment for infections such as HIV, HPV, and hepatitis. Such programs significantly increase testing volumes, promote awareness, and encourage collaboration between public health authorities and diagnostic providers, strengthening overall market demand.

Challenges in the Europe STD Diagnostics Market

Fragmentation of Healthcare Systems

One of the primary challenges facing the European STD diagnostics market is the fragmented nature of healthcare systems across countries. Regulatory frameworks, reimbursement policies, approval timelines, and procurement practices vary significantly between nations. Diagnostic solutions approved and reimbursed in one country may face delays or barriers in others, increasing complexity for market entry and expansion.

This fragmentation can slow the adoption of innovative diagnostic technologies and limit economies of scale. Companies often prioritize larger or more lucrative markets, potentially delaying access in smaller or less-funded healthcare systems.

Small Diagnostics Companies’ Constraints and Social Barriers

Smaller diagnostic companies often face difficulties navigating Europe’s diverse regulatory and healthcare landscapes. Limited financial resources, complex approval processes, and varying reimbursement models create entry barriers, particularly for emerging technologies.

Additionally, despite progress in awareness and education, social stigma surrounding sexually transmitted diseases continues to affect testing uptake in certain regions. Cultural conservatism, lack of sexual health education, and fear of social judgment discourage individuals from seeking testing, particularly in rural or traditional communities. While self-testing and point-of-care diagnostics help address these barriers, social challenges remain a limiting factor for market growth.

Europe Syphilis Testing Market

The syphilis testing market in Europe is experiencing renewed focus due to rising infection rates and the severe consequences of untreated disease. Screening is emphasized in antenatal care, blood donation programs, and surveillance of high-risk populations. Laboratory-based serological tests remain the cornerstone of syphilis diagnosis, supported by confirmatory testing algorithms to ensure accuracy.

Rapid syphilis tests are increasingly used in outreach and community programs, enabling immediate referral to treatment. Prevention of congenital syphilis is a key public health priority, driving sustained demand for routine antenatal screening across Europe.

Europe HIV Testing Market

The Europe HIV testing market is mature yet steadily expanding, driven by prevention strategies, early diagnosis initiatives, and improved accessibility. Laboratory immunoassays remain widely used, while rapid tests and self-testing kits are gaining acceptance due to convenience and confidentiality.

Efforts to reduce undiagnosed HIV cases and ensure timely linkage to treatment fuel demand for innovative testing platforms. Advances that shorten diagnostic windows and improve detection accuracy further strengthen the market’s growth trajectory.

Europe STD Molecular Diagnostics Market

Molecular diagnostics represent the fastest-growing segment within the Europe STD diagnostics market. These technologies offer unmatched sensitivity and specificity, making them the preferred choice for diagnosing infections such as chlamydia and gonorrhea. Adoption is strongest in hospital laboratories and large diagnostic centers with high testing volumes.

Multiplex molecular platforms reduce testing costs and enhance efficiency by detecting multiple pathogens simultaneously. Despite higher initial capital investments, molecular diagnostics account for a significant share of market revenue and are expected to become increasingly widespread with ongoing automation and laboratory modernization.

Europe STD Rapid Point-of-Care Platform Market

Rapid point-of-care STD diagnostic platforms are gaining traction due to their ability to deliver results within a single patient visit. These solutions are particularly valuable in sexual health clinics, emergency departments, and mobile testing programs where follow-up rates may be low.

Continuous improvements in accuracy and reliability have increased clinical confidence in rapid testing platforms. Although cost considerations remain, the public health benefits of immediate diagnosis and treatment support growing adoption across Europe.

Europe STD Diagnostics Hospitals and Clinics Market

Hospitals and clinics represent the largest end-user segment in the Europe STD diagnostics market. Hospitals manage complex diagnostic cases and rely on high-throughput analyzers, while clinics prioritize rapid testing solutions to support efficient patient flow.

Interoperability with electronic medical record systems is an increasingly important purchasing criterion. The demand for reliable, scalable, and connected diagnostic platforms continues to drive investment among institutional healthcare providers.

France STD Diagnostics Market

France benefits from a well-structured healthcare system and strong government support for preventive care. National screening programs for HIV and syphilis ensure consistent demand for STD diagnostics. Centralized laboratories conduct advanced testing, while community health centers support large-scale screening initiatives.

Preventive healthcare policies encourage routine screening rather than symptom-based testing. France’s diagnostics market is mature, with growing emphasis on molecular technologies and self-testing solutions supported by national health insurance programs.

Germany STD Diagnostics Market

Germany represents one of the most technologically advanced STD diagnostics markets in Europe. Strong laboratory infrastructure, high healthcare expenditure, and emphasis on preventive care support widespread adoption of molecular and automated diagnostic platforms.

Private and hospital laboratories drive demand for high-performance systems, while public health campaigns emphasize the importance of early detection and prevention. Germany’s focus on quality, efficiency, and patient dignity continues to shape diagnostic innovation.

United Kingdom STD Diagnostics Market

The UK STD diagnostics market is closely aligned with public health objectives focused on early diagnosis and prevention. Sexual health clinics and screening programs generate high testing volumes, supporting demand for both laboratory-based and point-of-care diagnostics.

Innovation in molecular and rapid testing technologies enhances service delivery, although budget constraints influence procurement decisions. The market maintains steady growth through a balance of cost control, clinical outcomes, and technological advancement.

Russia STD Diagnostics Market

The Russian STD diagnostics market shows uneven development across regions. Urban centers feature advanced laboratory infrastructure, while rural areas rely on simpler and more cost-effective diagnostic solutions. Public health campaigns aimed at disease surveillance and early diagnosis are increasing awareness and testing demand.

Cost sensitivity and access challenges favor flexible and affordable diagnostic platforms. Ongoing efforts to improve surveillance systems present growth opportunities for STD diagnostics across the country.

Europe STD Diagnostics Market Segmentation Analysis

By Test Type

Chlamydia Testing

Gonorrhea Testing

Syphilis Testing

HPV Testing

HSV Testing

HIV Testing

Trichomonas Testing

Mycoplasma genitalium Testing

Chancroid Testing

By Technology

Immunoassay-Based Methods

Molecular Diagnostics

Next-Generation Sequencing

Biosensor, Microfluidics, and Other Emerging Platforms

By Location of Testing

Central and Hospital Laboratories

Rapid Point-of-Care Platforms

Over-the-Counter and Home Self-Testing

By End User

Hospitals and Clinics

Diagnostic Laboratories

Home Care and OTC

By Country

France, Germany, Italy, Spain, United Kingdom, Belgium, Netherlands, Russia, Poland, Greece, Norway, Romania, Portugal, and Rest of Europe.

Competitive Landscape and Company Analysis

The Europe STD diagnostics market is highly competitive, with global and regional players focusing on innovation, portfolio expansion, and regulatory compliance. Key companies operating in the market include Abbott Laboratories, F. Hoffmann-La Roche AG, Hologic Inc., Becton Dickinson and Company, Danaher Corporation, Siemens Healthineers AG, bioMérieux SA, Thermo Fisher Scientific Inc., Qiagen N.V., and Bio-Rad Laboratories Inc.. Competitive analysis typically includes company overviews, leadership profiles, recent developments, SWOT analysis, revenue performance, and strategic positioning.

Europe STD Diagnostics Market Outlook and Future Trends

The Europe STD diagnostics market is set for robust growth through 2034, driven by rising disease prevalence, expanding screening programs, and continuous technological innovation. While challenges such as healthcare fragmentation and social stigma persist, advancements in molecular diagnostics, rapid testing, and self-testing solutions are transforming disease detection and management. Strong public health commitment, digital integration, and preventive care strategies will continue to position STD diagnostics as a critical component of Europe’s healthcare landscape.

renubresearch