France Convenience Store Market Size and Forecast 2026–2034

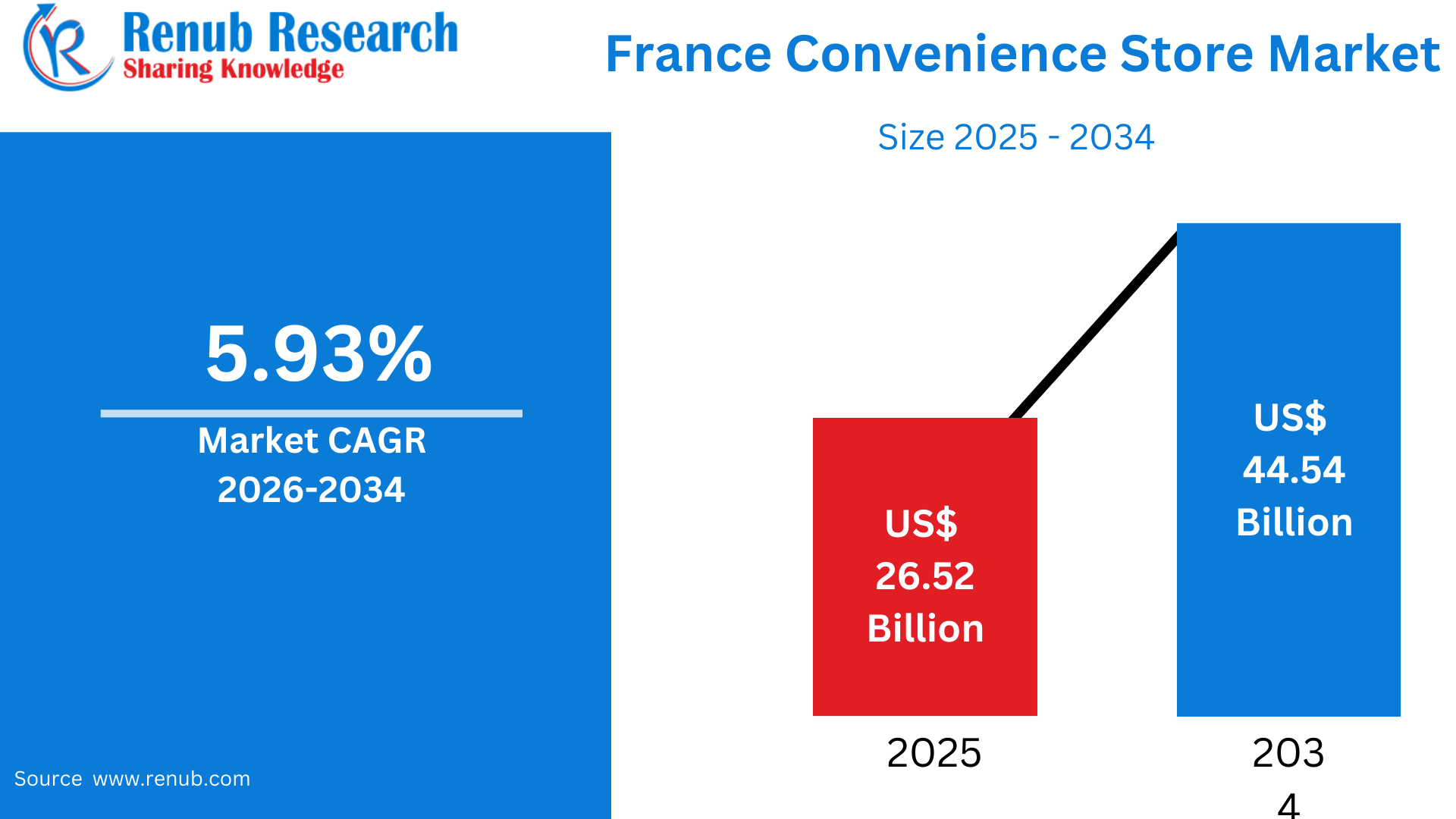

According To Renub Research France convenience store market is set to witness steady and sustained growth during the forecast period, expanding from a value of USD 26.52 billion in 2025 to approximately USD 44.54 billion by 2034. This growth represents a strong compound annual growth rate (CAGR) of 5.93% from 2026 to 2034. The upward trajectory of the market is supported by increasing urbanization, rising demand for quick and flexible shopping formats, and growing consumer preference for ready-to-eat and on-the-go food products.

Additional factors such as strong tourism inflows, extended store operating hours, and rapid adoption of digital and contactless payment methods are enhancing the appeal of convenience stores across France. As lifestyles become faster and consumers prioritize accessibility and efficiency, convenience stores are evolving into an essential component of the French retail ecosystem.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=france-convenience-store-market-p.php

Outlook of the Convenience Store Market in France

Convenience stores are compact retail outlets strategically located to provide quick access to essential daily-use products. These stores typically offer snacks, beverages, packaged foods, ready-to-consume meals, household items, and personal care products. Their defining characteristics include ease of access, proximity to consumers, extended operating hours, and fast checkout experiences. In France, convenience stores are commonly found in city centers, residential neighborhoods, transportation hubs, tourist zones, and near workplaces.

Changing lifestyles and dense urban living have significantly increased the relevance of convenience retailing in France. Professionals, students, commuters, and tourists increasingly rely on nearby stores for immediate purchases rather than large weekly supermarket trips. The rise in single-person households and smaller family units further strengthens demand for frequent, low-volume shopping. To meet evolving preferences, French convenience stores now emphasize fresh bakery items, organic snacks, locally sourced products, and premium ready-to-eat meals, blending speed with quality.

Urbanization and Shift Toward Faster Purchasing Behavior

Urbanization is one of the most powerful drivers of the convenience store market in France. With more than 80% of the population living in urban areas, cities such as Paris, Lyon, Marseille, and Toulouse are experiencing higher population density and busier lifestyles. As commuting times increase and work-life schedules become more demanding, consumers are moving away from time-intensive hypermarket shopping toward faster, more flexible purchasing options.

Convenience stores cater effectively to this demand by offering essential goods close to homes, offices, and transit points. Short shopping trips, extended evening hours, and weekend accessibility make these stores highly attractive. Dual-income households and young professionals particularly value the ability to quickly purchase meals, snacks, or necessities without disrupting their daily routines, reinforcing the importance of neighborhood-based retail formats.

Rising Demand for Ready-to-Eat, Fresh, and Local Food

The growing preference for ready-to-eat, fresh, and locally sourced food is a major growth catalyst for the French convenience store market. Modern consumers seek high-quality meal solutions that fit into busy schedules without compromising taste, freshness, or nutritional value. As a result, convenience stores increasingly stock freshly prepared sandwiches, salads, fruit portions, chilled meals, organic snacks, and regional specialties.

This trend aligns well with France’s strong culinary culture, which places high value on food quality and authenticity. Many convenience stores collaborate with local bakeries, farms, and artisan suppliers to differentiate themselves from mass-market supermarkets. Demand for sustainable packaging, natural ingredients, and minimally processed foods further shapes product assortments. The ability to offer premium yet convenient food options positions convenience stores as trusted local food destinations rather than just impulse-buy outlets.

Technology Adoption and Digital Payments

Digital transformation is reshaping the convenience store landscape in France. Widespread adoption of contactless and card-based payments has significantly improved transaction speed and customer convenience. Many stores now integrate self-checkout systems, digital loyalty programs, and mobile payment options to reduce queues and enhance the shopping experience.

Omnichannel strategies are also gaining traction. Click-and-collect services allow customers to place orders online and pick them up in-store within minutes. Partnerships with food delivery platforms enable stores to extend their reach beyond physical footfall. As French consumers increasingly prefer digital payments over cash, technology-enabled convenience stores are better positioned to improve efficiency, reduce operational friction, and strengthen customer loyalty.

High Operational Costs and Competitive Pressure

Despite strong growth prospects, the French convenience store market faces notable challenges. Operating costs remain high, particularly in urban areas where rents, wages, and utility expenses are significant. Limited store space restricts product assortment and storage capacity, making inventory management more complex.

Competition from supermarkets and hypermarkets adds further pressure, especially as large retail chains expand into smaller urban store formats. These competitors benefit from economies of scale that allow more aggressive pricing. In addition, strict regulations related to labor laws, operating hours, food safety, and pricing policies increase compliance costs. Balancing affordability, product diversity, and profitability remains a key challenge for convenience store operators.

Supply Chain Complexity and Fresh Food Management

Maintaining a consistent supply of fresh and perishable goods is another major operational challenge for convenience stores in France. High consumer expectations regarding freshness require frequent restocking and efficient inventory turnover. Small storage areas increase the risk of stockouts or food waste, particularly for produce, dairy, and ready-to-eat meals.

Urban logistics further complicate supply chains, with congestion, delivery restrictions, and higher transportation costs affecting reliability. Weather conditions and supplier variability can also disrupt availability. Minimizing spoilage while maintaining quality is critical, making advanced inventory management systems and strong supplier relationships essential for sustained performance.

France Raw Food Convenience Store Market

The raw food segment is gaining traction within French convenience stores as consumers seek natural, minimally processed ingredients for quick home cooking. Products such as fresh fruits, vegetables, herbs, and basic cooking essentials appeal to health-conscious shoppers.

Convenience stores leverage partnerships with local farmers and suppliers to promote freshness and regional sourcing. Efficient refrigeration, attractive packaging, and frequent replenishment help maintain quality despite limited space. This segment aligns with the growing trend of “quick-cooking,” where consumers prepare simple, healthy meals using readily available raw ingredients purchased close to home.

France Frozen Food Convenience Store Market

Frozen food represents a strong and profitable segment within the French convenience store market. Its longer shelf life, reduced waste, and consistent quality make it well-suited to small retail formats. Popular products include frozen vegetables, ready meals, desserts, and bakery items.

Advancements in freezing technology have improved taste and texture, increasing consumer confidence in frozen offerings. High-quality frozen foods appeal to consumers seeking convenience without sacrificing flavor. This category allows convenience stores to balance freshness expectations with operational efficiency, supporting stable margins and reduced spoilage.

France Meat and Poultry Products Convenience Store Market

Packaged meat and poultry products form an important category for convenience stores catering to small households. Ready-to-cook chicken, marinated meats, and deli products are popular among consumers seeking quick meal preparation options.

Given France’s strong emphasis on food quality, stores prioritize reliable sourcing and strict temperature control. While handling perishable meat products presents challenges, consistent demand driven by smaller family sizes and convenience-oriented cooking habits sustains this segment’s relevance.

France Cereal-Based Products Convenience Store Market

Cereal-based products are a cornerstone of convenience store offerings in France. Bread, pastries, cereals, biscuits, snack bars, and bakery items reflect the country’s deep-rooted baking traditions. Fresh baguettes, croissants, and viennoiseries are often supplied daily through partnerships with local bakeries.

Packaged cereals and snack products cater to health-conscious consumers and busy professionals. This segment supports both impulse purchases and daily meal solutions, reinforcing the role of convenience stores as everyday food providers.

Paris Convenience Store Market

Paris represents the most dynamic convenience store market in France due to its dense population, fast-paced lifestyle, and strong tourism activity. Convenience stores located near metro stations, offices, and residential areas benefit from high foot traffic throughout the day.

Parisian consumers expect high-quality, fresh, organic, and premium products, driving continuous upgrades in product assortments. Extended operating hours and proximity to tourist attractions further enhance sales of ready meals, beverages, and daily necessities, making Paris a benchmark market for convenience retail innovation.

Marseille Convenience Store Market

The convenience store market in Marseille is shaped by its Mediterranean lifestyle, multicultural population, and port-based economy. Stores cater to diverse tastes, offering fresh produce, value-driven ready meals, and international cuisine influences.

Locations near beaches, transport hubs, and tourist areas experience seasonal demand peaks. While affordability remains important, consumers place strong emphasis on freshness and authenticity. Urban development and commuting patterns continue to support market expansion.

Strasbourg Convenience Store Market

Strasbourg benefits from its role as an administrative center, student hub, and cross-border city. High pedestrian traffic and international visitors drive demand for convenience foods, bakery products, and ready-to-eat meals.

The proximity to Germany influences demand for organic, eco-friendly, and health-oriented products. Compact urban planning supports dense neighborhood store networks, making convenience stores an integral part of daily life for residents and visitors alike.

Market Segmentation Overview

The France convenience store market is segmented by type into raw food, canned food, frozen food, ready-to-eat, ready-to-cook, and other categories. Product segmentation includes meat and poultry products, cereal-based products, vegetable-based products, and others.

Distribution channels include supermarkets and hypermarkets, convenience stores, specialty stores, and other retail formats. Geographically, the market spans major cities such as Paris, Lyon, Marseille, Toulouse, Bordeaux, Lille, Nantes, Strasbourg, Nice, and Montpellier, along with the rest of France.

Competitive Landscape and Company Analysis

The French convenience food and retail ecosystem is supported by global and regional food manufacturers supplying packaged, frozen, and ready-to-eat products. Key companies operating within the broader convenience store supply chain include Ajinomoto Co., Inc., Amy’s Kitchen, Inc., Cargill, Incorporated, Conagra Brands, Inc., General Mills, Inc., Nestlé SA, and Tyson Foods Inc..

These companies support the market through product innovation, supply chain reliability, and alignment with evolving consumer preferences. Competitive analysis typically includes company overviews, leadership insights, recent developments, SWOT analysis, and revenue performance.

Conclusion

The France convenience store market is poised for robust growth through 2034, driven by urbanization, lifestyle changes, demand for fresh and ready-to-eat foods, and rapid digital adoption. While operational costs and supply chain complexity pose challenges, innovation in product offerings, technology integration, and localized sourcing continues to strengthen the sector.

As convenience becomes a defining factor in modern French consumer behavior, convenience stores are evolving into essential neighborhood retail hubs, positioning the market for long-term resilience and expansion.

renubresearch